|

1

|

- © Copyright 1978-2007 Ben Livson, BAL Consulting P/L™.

All rights reserved.

|

|

2

|

- When you can measure what you are speaking about, and express it in numbers, you know

something about it: but when you cannot express it in numbers, your

knowledge is of a meagre and unsatisfactory kind: it may be the

beginning of knowledge, but you have scarcely, in your thoughts,

advanced to the stage of science.

|

|

3

|

- Human Capital: Competencies, Attitude …

- Structural Capital

- Policies, Procedures and Processes

- Corporate Databases

- Content

- Intellectual Property: Patents, Licenses …

- Customer Capital

- Marketing, Sales and Delivery Channels

- Customer Relationship

- Partnerships and Alliances

|

|

4

|

|

|

5

|

|

|

6

|

- Economic Value-Added (EVA) =

- Accounting Profit – Cost of

Shareholder Capital

|

|

7

|

|

|

8

|

|

|

9

|

|

|

10

|

|

|

11

|

|

|

12

|

- Book Value Accounting still based on Luca Pacioli’s 1494 Summa de

Arithmetica, Geometrica, Proportioni et Proportionalita treatise on

double-entry bookkeeping also known as the Italian Method.

|

|

13

|

|

|

14

|

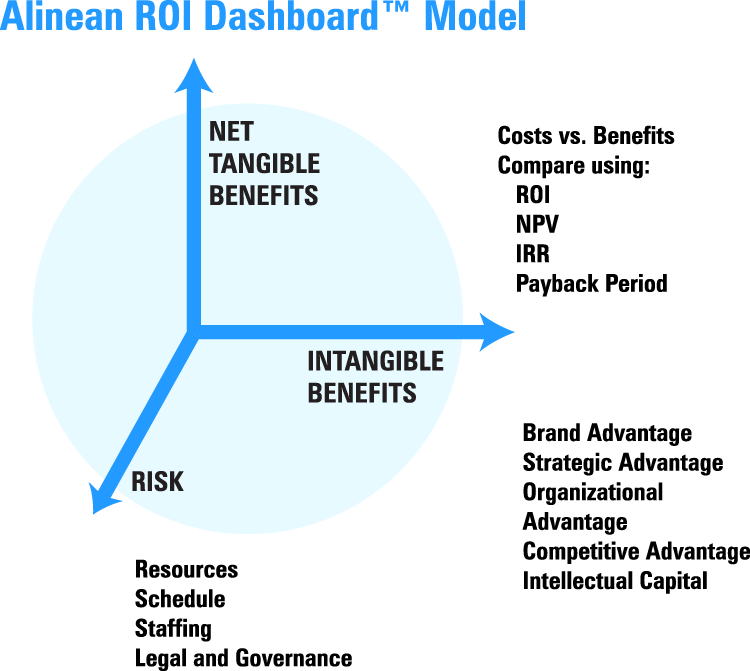

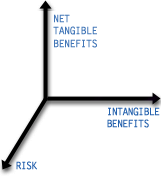

- $People Brand Advantage

- $Process Strategic Advantage

- $Content Organizational Advantage

- $Brand Mapping of Intangibles

- $Alliances Competitive Advantage

- $Customers Risk Reduction

- $IP Intellectual Property

|

|

15

|

|

|

16

|

|

|

17

|

- Knowledge Capital = (Normalized earnings - earnings from tangible and

financial assets)/(Knowledge capital discount rate)

- Strengths: Valuation is forward looking. It has some predictive

capability.

- Weaknesses: Requires more effort to apply.

|

|

18

|

- Intellectual Capital = Market Value (Price/Share x # of shares) - Book

Value (Equity - Debt)

- Strassmann’s Knowledge Capital = (Profits - Financial Capital

"Rental")/(interest rate cost of long term debt)

- Tobin’s Q = Market Value/Replacement Cost

|

|

19

|

- Calculate average pre-tax earnings for three years

Calculate average year-end tangible assets for 3 years

Divide earnings by assets --> company average ROA for 3

years

Find industry average ROA

Multiply industry ROA by company's tangible assets. Subtract

product from

company's pre-tax earnings. --> Excess return.

Calculate 3 year average tax rate. Multiply by excess

return

Subtract from excess return --> premium attributable to

intangible assets.

Calculate Net Present Value of Premium. Divide premium by

discount rate. (i.e., cost of capital)

|

|

20

|

- MC=Market Capital, KC=Knowledge Capital, BV=Book Value &

CV=Comprehensive Value and PV=Perception Value in market perception

- CV=BV+KC

- MC=CV+PV=BV+KC+PV

- Nokia 2000: MC=$160b=$6b+$94b+$60b

- High PV=>Overvalued; Low PV => Undervalued

- Best Stock: Low PV and High KC !

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}